New Delhi: As India kicks off local manufacturing of semiconductors to cut dependency on China, the shortage of raw material amid the Russia-Ukraine war which, if lingers for a longer period of time, may hamper the country’s dream to produce high-end semiconductors and become their global hub.

The government recently set up the India Semiconductor Mission (ISM) and approved Rs 76,000 crore ($10 billion) for the development of semiconductors and display manufacturing ecosystem in the country.

The Rs 76,000 crore Production-Linked Incentive (PLI) scheme will be spread across six years. As part of the scheme, incentives worth Rs 2.3 lakh crore will be provided to position India as a global hub.

With geopolitical tensions now extending from Asia to Europe and from semiconductor manufacturing to raw material supply, Indian players need to re-evaluate capacity expansion and investment decisions, say experts.

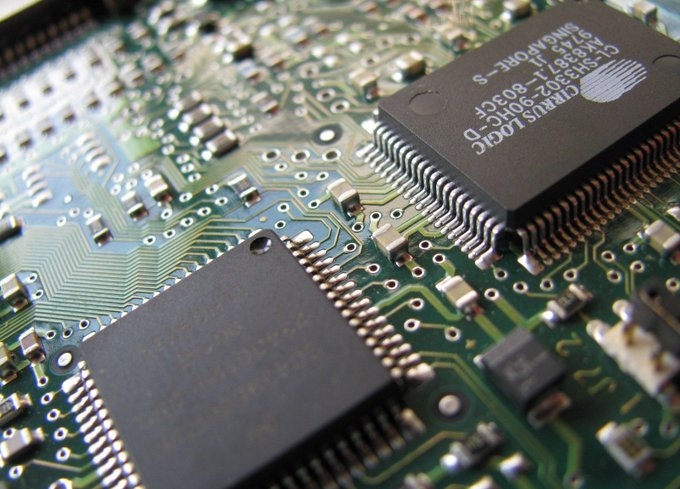

Some raw materials exported from Russia and Ukraine, such as rare gas neon, chemical C4F6 and metals palladium, nickel, platinum, rhodium and titanium are critical for semiconductor manufacturing.

Palladium is used in component production, like for the substrate in PCB.

However, precious metals such as palladium, platinum and rhodium are mainly used in the catalytic converters for vehicles, according to Counterpoint Research.

Titanium nitride (TiN) is a widely used material for semiconductor manufacturing as a diffusion barrier.

According to experts, black swan events, such as the ongoing war, have the potential to cause a significant strain on global supply chains, including potentially impacting chip capacity and spiking chip prices.

“In an interconnected and intertwined world, India will also face some direct or indirect impact in its electronics manufacturing,” Prabhu Ram, Head-Industry Intelligence Group, CMR, told IANS.

The unavailability of crucial upstream raw materials — such as semiconductor-grade neon or palladium — “could have a cascading impact through the supply chain, and impacting especially those manufacturers in Asia, who are reliant on Ukraine”, Ram said.

The PLI and the scheme for promotion of manufacturing of electronic components and semiconductors (SPECS), among others, have triggered the shift of manufacturing from other countries to India.

In such a scenario, raw material shortage may derail the country’s dream.

Pankaj Mohindroo, Chairman of India Cellular and Electronics Association (ICEA), said that there should be no major impact on the semiconductor market in the country due to the Ukraine crisis.

“However, since oil prices have gone up, several commodities are becoming costlier. Overall, the consumer electronics industry may face a short-term price fluctuation if the prices of raw material that come from Ukraine keep going up and the situation does not stabilise soon,” Mohindroo told IANS.

According to Brady Wang from Counterpoint Research, small and medium chipmakers and allied businesses may face increased supply pressure owing to exhausted inventories and the difficulty in connecting with new sources if the conflict continues.

“Rapidly rising metal (nickel and palladium) prices will represent a new impediment to the revival of the automotive market if the conflict continues,” he said.

In the medium term, the lack of the aforementioned raw materials will have little influence on semiconductor producers. The situation will be managed through existing inventory and other suppliers.

However, it is inevitable that prices will rise significantly.

“If the conflict persists, supply chain uncertainty will keep raw material inventories at higher levels for a longer length of time. Supply chain management will become more complicated as well,” Wang noted.

The worldwide chip shortage will exist well into the last part of 2022, and possibly even 2023, according to the latest US Commerce Department report on semiconductor supply chain.

Manufacturers have already seen their stocks of semiconductors plunge amid the global chip shortage.

A recent survey of more than 150 firms found that supplies had fallen from an average of 40 days’ worth in 2019 to just five days in late 2021.

IANS

{kind=link}